Every year, millions of Americans leave hard-earned money on the table simply because they do not fully grasp the mechanics of their benefits package. While nearly 82% of dental policies in the United States are PPO dental insurance plans, a staggering number of policyholders fail to maximize their annual maximums. They often navigate complex fee schedules incorrectly or misunderstand the fundamental nature of the product.

Table of Contents

Dental coverage is not “insurance” in the traditional sense of protecting against a catastrophic financial loss, like a house fire or a car accident. Instead, it functions as a pre-paid benefit with a strict financial cap. It is designed to offset the cost of maintenance rather than cover it entirely.

To get the most out of your premiums, you need to understand the rigid framework of codes, clauses, and classifications that insurers use to adjudicate claims. This guide breaks down the fee schedules, the hidden exclusions, and the strategies industry insiders use to reduce out-of-pocket expenses. We will explore the nuances of network leasing, the mathematics of claim adjudication, and the tactical moves you can make during open enrollment.

Quick Answer: What is PPO Dental Insurance?

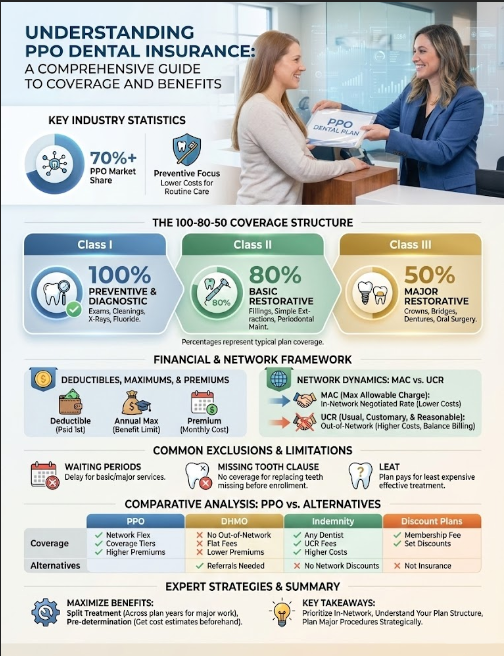

PPO (Preferred Provider Organization) dental insurance is a managed care plan that offers members access to a network of dentists who have agreed to reduced fee schedules. Unlike HMOs, PPO plans allow you to visit any dentist you choose. However, you receive significantly higher coverage and lower out-of-pocket costs when visiting an in-network dentist. These plans typically follow a 100-80-50 coverage structure with an annual maximum benefit limit. The primary value proposition is the balance between provider choice and cost control.

Key Industry Statistics

- 82%: The percentage of commercial dental policies that are PPO plans (NADP).

- $1,500: The standard annual maximum. This figure has barely changed since the 1970s despite inflation.

- $300 Million+: Estimated amount of dental benefits lost annually due to unused maximums.

- 30-40%: The average discount off street rates negotiated by PPO carriers for in-network services.

- 6-12 Months: The typical waiting period for major restorative work on individual plans.

- 50%: The typical coinsurance rate for major procedures like crowns and bridges.

The Anatomy of a PPO Plan: Understanding the 100-80-50 Structure

Almost all dental insurance plans operating under the PPO model use a tiered reimbursement system known as the “100-80-50” structure. This format is not accidental. It is mathematically designed to incentivize preventive care while sharing the cost burden for more expensive, neglect-based procedures. Understanding which “Class” your procedure falls into is the first step in predicting your bill. The classification of services is dictated by CDT (Current Dental Terminology) codes, which are maintained by the American Dental Association.

Class I: Preventive and Diagnostic Services (100% Coverage)

Insurers cover these services at 100% because they are statistically proven to reduce long-term costs for the carrier. If a carrier pays $100 for a cleaning today, they avoid paying $1,200 for a root canal and crown five years later. In most PPO structures, the deductible is waived for Class I services. This means you can walk in, get your cleaning, and walk out without opening your wallet, assuming you stay in-network.

- Prophylaxis (D1110): Routine cleanings. These are typically covered twice per calendar year or once every six months.

- Periodic Oral Evaluation (D0120): The standard exam performed by the dentist during your hygiene visit.

- Bitewing X-rays (D0274): Cavity-detecting radiographs. These are usually limited to one set per year.

- Fluoride Varnish (D1206): Topical application of fluoride. Note that many adult plans cut off coverage for this at age 14 or 18.

- Sealants (D1351): Protective coatings for molars. Like fluoride, this often has an age limit clause.

Expert Insight: While coverage is listed at 100%, this is 100% of the allowed amount. If you visit an out-of-network provider who charges above the customary rate, you may still owe a balance even for a “fully covered” cleaning. Always verify network status to ensure 100% truly means free.

Class II: Basic Restorative Services (80% Coverage)

Class II covers treatments for early-stage decay and gum disease. The patient is usually responsible for 20% of the negotiated fee plus the annual deductible. This category represents the “maintenance” phase of dentistry. It addresses problems that have moved beyond prevention but are not yet catastrophic.

- Restorations: Amalgam (silver) and composite (white) fillings. Note that some plans downgrade posterior white fillings to the silver rate.

- Simple Extractions (D7140): Removal of erupted teeth that do not require cutting into bone.

- Periodontal Scaling and Root Planing (D4341): Often called a “deep cleaning.” This is for treating active gum disease.

- Periodontal Maintenance (D4910): The cleanings you receive after gum disease treatment. These are often a point of contention and may be downgraded to standard cleanings.

- Emergency Palliative Treatment (D9110): A minor procedure to relieve pain during an emergency visit.

Nuance Alert: One of the biggest areas of confusion involves Endodontics (Root Canals). Some aggressive PPO dental insurance plans categorize root canals as Class II (Basic). However, many modern plans push them to Class III (Major). Always verify this classification. The difference between 80% coverage and 50% coverage on a $1,200 procedure is substantial.

Class III: Major Restorative Services (50% Coverage)

This category includes high-cost procedures meant to replace missing teeth or restore heavily damaged ones. The carrier pays 50%, and the patient pays 50%. This creates a significant financial barrier, which is intentional. Insurers want to discourage patients from needing these services through neglect. They also want to limit their financial exposure.

- Prosthodontics: Bridges, partial dentures, and full dentures.

- Single Crowns (Caps): Required when a tooth lacks sufficient structure for a filling. This includes code D2740 (Porcelain Crown).

- Onlays and Inlays: Lab-fabricated fillings that cover a larger portion of the tooth.

- Surgical Implants (D6010): While historically excluded, more modern plans are beginning to cover implants under Class III. They often come with a separate lifetime maximum.

- Complex Oral Surgery: Removal of impacted wisdom teeth often falls here. However, it may sometimes fall under medical insurance depending on the specific pathology.

The Financial Framework: Deductibles, Maximums, and Premiums

To effectively manage your dental care budget, you must look past the monthly premium. You need to examine the limitations embedded in the contract. The premium is merely the entry fee. The real costs are determined by the deductible, the maximum, and the fee schedule.

The Deductible Explained

The deductible is the amount you must pay out-of-pocket before the insurance company contributes to the cost of Class II or Class III services. The industry standard is $50 for an individual and $150 for a family. This number has remained surprisingly low and consistent for decades.

Most plans operate on a “Calendar Year” basis (January 1 to December 31). If you have a procedure done on December 28th and pay your $50 deductible, it resets on January 1st. You must pay it again for your next visit in the new year. A minority of plans operate on a “Plan Year.” This might start the month you signed up or the month your employer’s fiscal year begins. Knowing your reset date is crucial for financial planning.

The Annual Maximum Cap

This is the most critical limitation of dental insurance. Unlike medical insurance, which has an out-of-pocket maximum (limiting what you pay), dental insurance has an annual maximum (limiting what they pay). This flips the risk model entirely.

The standard annual maximum is typically between $1,000 and $1,500. Once the insurance company has paid out this amount on your behalf, you are responsible for 100% of all subsequent costs for the remainder of the year. Inflation has severely eroded the value of this benefit. A $1,000 maximum in 1980 could cover multiple crowns and a root canal. Today, a single root canal and crown can easily exceed $2,000, exhausting the maximum instantly.

Rollover Benefits

Some progressive carriers have introduced “rollover” or “max-builder” features. If you visit the dentist for preventive care but use less than a specific threshold of your maximum (e.g., less than $500), the carrier allows you to roll over a portion of the unused funds to the next year. This can eventually boost your annual maximum from $1,500 to $3,000 or more. This provides a valuable safety net for unexpected major dentistry in future years.

Network Dynamics: The Critical Difference Between MAC and UCR

This section explains the mathematical mechanism that determines your bill. Understanding the difference between Maximum Allowable Charge (MAC) and Usual, Customary, and Reasonable (UCR) fees is essential. It is the only way to avoid surprise bills.

In-Network: The MAC Model

When you see an in-network dentist, you are protected by a contract. The dentist has signed an agreement with the carrier (e.g., Delta Dental, Cigna, MetLife) to accept a specific fee schedule. This is known as the Maximum Allowable Charge (MAC).

For example, imagine a dentist’s standard office fee for a crown is $1,400. However, the PPO negotiated rate is $900. The dentist must write off the $500 difference. They cannot bill you for it. Your 50% co-insurance is calculated based on the $900, not the $1,400. This “contracted write-off” is often more valuable than the actual insurance check. It acts as a guaranteed discount regardless of your remaining maximum.

Out-of-Network: The UCR Model

When you use out-of-network coverage, the dentist has no contract to write off fees. The insurance company will pay a percentage based on what they deem is the “Usual, Customary, and Reasonable” (UCR) fee for that zip code. This is where patients get into trouble.

The problem arises because insurance data is often outdated or deliberately suppressed. If the insurer claims the UCR for a crown is $1,000, but the dentist charges $1,400, the insurance pays 50% of $1,000 ($500). You owe your 50% ($500) plus the $400 difference that the insurance didn’t recognize. This is called “Balance Billing.” It effectively destroys the value of your coverage.

Cost Comparison: Porcelain Crown (D2740)

| Cost Component | In-Network (PPO) | Out-of-Network |

|---|---|---|

| Dentist’s Standard Fee | $1,400 | $1,400 |

| Negotiated / Allowed Fee | $900 (MAC) | $1,000 (UCR) |

| Contracted Write-off | -$500 | $0 |

| Insurance Pays (50%) | $450 | $500 |

| Patient Co-insurance (50%) | $450 | $500 |

| Balance Bill | $0 (Prohibited) | $400 |

| TOTAL PATIENT COST | $450 | $900 |

The “Fine Print”: Exclusions, Clauses, and Limitations

As a consultant reviewing denied claims, I frequently encounter patients who are shocked to learn their “comprehensive” PPO dental insurance plan has specific clauses excluding their needed treatment. The devil is truly in the details. Here are the most common pitfalls that lead to claim denial.

Waiting Periods

Employer-sponsored plans often waive waiting periods as a perk of the group contract. However, individual plans purchased on the open market almost always include them. The standard waiting period is 6 months for Class II (fillings) and 12 months for Class III (crowns/bridges). This protects the insurer from “adverse selection.” This is the industry term for people buying insurance only when they know they need expensive work. If you have had continuous coverage with a previous carrier, you can often request a “waiting period waiver.” You do this by providing a Certificate of Creditable Coverage from your previous insurer.

The Missing Tooth Clause (MTC)

This is arguably the most frustrating exclusion for patients. The clause states that the policy will not pay to replace a tooth that was extracted before the policy went into effect. If you lost a tooth five years ago and buy insurance today hoping to get a bridge or implant, the claim will be denied. The insurer views the missing tooth as a “pre-existing condition.” They will only pay to replace teeth that are extracted while you are covered under their specific plan.

Least Expensive Alternative Treatment (LEAT)

Also known as the “downgrade” clause, this allows the insurance company to reimburse the service based on the cheapest viable option. The most common example involves composite (white) fillings on molars. While the dentist places a white filling, the insurance company may only pay the rate of an amalgam (silver) filling. You are responsible for the difference in cost. This does not mean you must get the silver filling. It simply means the insurance subsidy is capped at the lower rate. Another common downgrade is paying for a partial denture instead of a fixed bridge.

Frequency Limitations

Even if you have remaining annual maximum dollars, frequency rules may block a claim. These rules dictate how often a specific procedure can be repeated.

- Cleanings: Often limited to “2 per calendar year” or “1 every 6 months.” The latter is stricter; if you go a day early, it is denied.

- Crowns: Typically replaced only once every 5 to 7 years on the same tooth. If a crown breaks after 4 years, the replacement is on you.

- Full Mouth X-rays: Usually covered once every 3 to 5 years.

- Fillings: Generally once every 24 months on the same surface of the same tooth.

Alternate Benefit Clause

This is similar to the LEAT clause but broader. It gives the insurer the right to pay for a “professionally acceptable” alternative treatment if it is cheaper. For example, if you opt for a high-end zirconia crown, the plan might only pay for a standard metal-fused-to-porcelain crown. You pay the upgrade cost.

Comparative Analysis: PPO vs. Other Dental Models

How does PPO dental insurance stack up against other market options? The choice usually comes down to a trade-off between provider choice and premium cost. Understanding the alternatives helps clarify why PPO is the dominant model.

PPO vs. DHMO (HMO)

Dental Health Maintenance Organizations (DHMOs) operate on a capitation model. The dentist is paid a small monthly fee for every patient assigned to their office, regardless of whether the patient is seen. There are no annual maximums and premiums are low, but the network is very small. Dentists in HMOs are often volume-driven because the capitation checks are small. They must see many patients to remain profitable. In contrast, PPO plans offer a vast network and reimbursement rates that allow dentists to spend more time per patient.

PPO vs. Indemnity Plans

Indemnity plans are the “old school” fee-for-service models. They have no network limitations. You can go to any dentist, and the plan pays a percentage of UCR. These plans are rare today because they are expensive for employers. They offer the ultimate freedom but often require the patient to pay upfront and wait for reimbursement. PPO plans have largely replaced them due to cost control mechanisms.

PPO vs. Discount Plans

Discount plans are not insurance. They are membership clubs where you pay a yearly fee to access a network of dentists who have agreed to reduced rates. There are no claims to file, no waiting period, and no annual maximums. However, you pay the full discounted rate out of pocket. These are excellent for patients who have exhausted their maximums or need cosmetic work not covered by insurance.

| Feature | PPO Plan | DHMO (HMO) | Indemnity Plan |

|---|---|---|---|

| Provider Choice | High (In & Out of Network) | Restricted (Must be assigned) | Unlimited |

| Premiums | Moderate | Low | High |

| Waiting Periods | Common (Individual Plans) | Rare | Common |

| Balance Billing Risk | Low (if In-Network) | None (Fixed Copays) | High |

Expert Strategies for Maximizing Your PPO Benefits

Navigating dental insurance plans requires strategy. It is not a passive product. Here are proven methods to extract more value from your policy and avoid leaving money on the table.

The “Split Treatment” Strategy

If you require extensive work, such as two crowns and a bridge, the cost will likely exceed your annual maximum. If your dental health permits, schedule the first phase of treatment in December and the second phase in January. This allows you to use the current year’s maximum for the first half and the new year’s maximum for the second half. You effectively double your available benefits for a single treatment plan. This requires careful coordination with your dentist’s front office.

The Pre-determination of Benefits

Never rely on a verbal estimate for expensive procedures. Ask your dental office to file a “Pre-determination of Benefits” (also called a Pre-Estimate or Pre-Auth). The dentist sends the proposed treatment plan, codes, and X-rays to the carrier before the work begins. The insurance company reviews the clinical evidence and sends back a written statement. This document details exactly what they will pay and what they will deny. This protects you from “medical necessity” denials after the work is done. It is particularly vital for 100-80-50 coverage items in the 50% category, where rejection is costly.

Coordination of Benefits (Dual Coverage)

If you are covered by two PPO plans (e.g., your employer and your spouse’s employer), you have “dual coverage.” However, this does not automatically mean 100% coverage. Most modern plans have “Non-Duplication of Benefits” clauses. If your primary plan pays 80%, and the secondary plan also covers 80%, the secondary may pay nothing because the primary already exceeded the secondary’s liability. This is also known as a “Carve-Out” clause.

To determine which plan is primary, insurers use the “Birthday Rule.” The plan of the spouse whose birthday falls earlier in the calendar year (month/day) is primary for dependent children. The year of birth does not matter. If the birthdays are identical, the plan that has been in effect longer is usually primary.

Utilizing Flexible Spending Accounts (FSA) and HSAs

Dental expenses are eligible for payment via FSAs and HSAs. This allows you to pay your deductibles and coinsurance with pre-tax dollars. This effectively saves you 20% to 30% depending on your tax bracket. For large treatment plans like Invisalign or implants, coordinating your HSA funds with your PPO coverage is a powerful financial move.

Reading Your Explanation of Benefits (EOB)

After every visit, you will receive an Explanation of Benefits (EOB). This is not a bill. It is a receipt of how the claim was processed. Learning to read this document is crucial for spotting errors.

Look for the column labeled “Patient Responsibility.” This should match the bill you received from the dentist. If the EOB says you owe $50, but the dentist billed you $150, there is a discrepancy. Check the “Remarks” or “Codes” section at the bottom. This is where the insurer explains why they denied a portion of the claim. Common remarks include “Frequency limit exceeded” or “Documentation does not support medical necessity.” If you see these, call your dentist immediately. They can often appeal the decision with a written narrative.

How to Choose the Best PPO Dental Plan

Not all PPO dental insurance policies are created equal. When selecting a plan during open enrollment, look deeper than the premium. A cheap plan with a restrictive network is often more expensive in the long run.

Assessing the Network

Large carriers like Cigna, Aetna, or Delta Dental often have multiple networks. For example, Delta Dental has “PPO,” “Premier,” and “DeltaCare.” A dentist might be in-network for the “Premier” list but out-of-network for the “PPO” list. The reimbursement rates differ significantly between these tiers. Verify your specific dentist’s status with the exact plan name, not just the carrier name.

Analyzing “Graduated Benefits”

Some insurers reward loyalty with graduated benefits. Coverage for major work might start at 25% in year one, rise to 50% in year two, and cap at 80% in year three. If you anticipate needing major work in the future but not immediately, these plans can be excellent investments. They discourage people from hopping between plans annually.

Checking for Rollover Features

As mentioned earlier, the rollover feature is a game-changer. If you have generally healthy teeth, prioritize a plan with this feature. It allows you to build a war chest of benefits for the year you finally need a crown or root canal. Without this feature, your unused $1,500 benefit disappears every December 31st.

The Future of PPO Dental Insurance

The dental insurance landscape is evolving. We are seeing a trend toward “Medical-Dental Integration.” Carriers are realizing that oral health impacts systemic health (diabetes, heart disease). Some PPO plans now offer extra cleanings for pregnant women or diabetics. This is a move toward value-based care.

Additionally, teledentistry is becoming a covered benefit. This allows for remote consultations for emergencies, which are often covered as Class I or Class II services. Keep an eye on your plan updates to take advantage of these new features.

Industry Reference & Data Integration

The landscape of dental benefits is monitored by several key organizations. According to the National Association of Dental Plans (NADP), the PPO model continues to dominate due to its balance of cost-containment and patient choice. Furthermore, the American Dental Association (ADA) regularly updates the CDT (Current Dental Terminology) codes. These codes dictate how procedures like implants and cleanings are categorized. Consumers can also use resources like the Fair Health Consumer database. This tool allows you to look up local UCR fees in your zip code to see if an out-of-network dentist’s fees are reasonable.

Summary & Key Takeaways

PPO dental insurance remains the most flexible and popular way for Americans to finance their oral health. However, it is a product defined by its limitations as much as its benefits. The key to success lies in staying with an in-network dentist to leverage the negotiated fee schedule. This is your primary shield against balance billing. Remember that the annual maximum is a “use it or lose it” benefit unless you have a specific rollover provision.

Before your next appointment, review your Summary of Plan Description (SPD). Knowing whether your root canal is a Basic or Major service can save you hundreds of dollars. Be aware of waiting periods if you are on a new plan. Treat your dental coverage as a discount coupon book rather than a blank check. Use the 100-80-50 coverage structure to plan your treatment timeline strategically. By understanding the rules of the game, you can transform your dental insurance from a source of frustration into a powerful financial tool.

Frequently Asked Questions

What exactly is PPO dental insurance and why is it the dominant plan type?

PPO (Preferred Provider Organization) dental insurance is a managed care model that balances provider choice with cost control. It accounts for 82% of the market because it offers access to a vast network of providers who agree to a Maximum Allowable Charge (MAC). Unlike an HMO, it allows you to see any dentist, though your out-of-pocket costs are significantly lower when staying in-network.

How does the 100-80-50 coverage structure impact my dental bills?

This is the standard tiered reimbursement framework used to adjudicate claims. Class I (Preventive) services like cleanings are typically covered at 100%. Class II (Basic) services like fillings are covered at 80%, and Class III (Major) services like crowns or bridges are covered at 50%. This structure is designed to incentivize maintenance and reduce the carrier’s long-term risk.

What is the difference between MAC and UCR fee schedules?

MAC (Maximum Allowable Charge) is the discounted fee an in-network dentist is contractually obligated to accept. UCR (Usual, Customary, and Reasonable) is the fee used for out-of-network claims. If you go out-of-network, you are subject to ‘balance billing,’ where you must pay the difference between the dentist’s street rate and the insurer’s UCR limit.

Why hasn’t the annual maximum benefit increased with inflation?

The standard annual maximum of $1,500 has remained largely stagnant since the 1970s. Because dental ‘insurance’ functions more as a pre-paid benefit than a catastrophic safety net, carriers use this cap to limit their financial exposure. Consequently, a single major restorative procedure like a root canal and crown can often exhaust your entire yearly benefit.

What is a waiting period and can I waive it?

A waiting period is a set time (usually 6–12 months) you must be enrolled before the carrier pays for Class II or Class III services. This prevents ‘adverse selection.’ You can often waive this period on new employer-sponsored plans or by providing a Certificate of Creditable Coverage proving you had continuous prior insurance.

How does the ‘Missing Tooth Clause’ (MTC) affect my coverage for implants?

The MTC is a common exclusion stating the insurer will not pay to replace a tooth that was extracted before the policy’s effective date. The carrier views the missing space as a pre-existing condition. If you lost a tooth years ago and want a bridge or implant now, the claim will likely be denied under this clause.

What is the LEAT or ‘downgrade’ clause in a PPO plan?

LEAT stands for Least Expensive Alternative Treatment. This clause allows insurers to reimburse a procedure based on the cheapest viable option. For example, if you receive a composite (white) filling on a molar, the insurer may ‘downgrade’ the payment to the rate of an amalgam (silver) filling, leaving you to pay the difference.

How can I use the ‘Split Treatment’ strategy to maximize my benefits?

If you require extensive work that exceeds your annual maximum, you can coordinate with your dentist to perform half the treatment in December and the other half in January. This allows you to apply the maximum benefit from two separate calendar years to a single treatment plan, effectively doubling your insurance subsidy.

Why should I request a Pre-determination of Benefits for major work?

A Pre-determination is a formal request where your dentist submits CDT codes and X-rays to the carrier before treatment begins. The carrier sends back a written statement detailing exactly what they will pay. This is the only way to guarantee the insurer agrees with the ‘medical necessity’ of the procedure and to avoid surprise bills.

What is the ‘Birthday Rule’ in coordination of benefits?

When a child is covered by two PPO plans (dual coverage), the Birthday Rule determines which plan is primary. The plan of the parent whose birthday (month and day) falls earlier in the calendar year pays first. Note that ‘Non-Duplication of Benefits’ clauses may still prevent the secondary plan from covering the remaining balance.

What are rollover or ‘max-builder’ benefits?

Some modern PPO plans reward policyholders for visiting the dentist. If you receive preventive care and use only a small portion of your annual maximum, the carrier ‘rolls over’ a portion of the unused funds into the next year. This allows you to eventually increase a $1,500 maximum to $3,000 or more for future major needs.

How do PPO plans compare to DHMO (HMO) models?

PPO plans offer much larger networks and higher reimbursement rates, which typically correlates with more time spent per patient. DHMOs use a capitation model with no annual maximums and lower premiums, but they severely restrict provider choice and often require dentists to work at higher volumes to remain profitable.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Dental insurance policies vary significantly by provider and state. Always consult with a licensed insurance agent or your human resources department before making enrollment decisions, and speak with your dental provider regarding specific treatment costs.

References

- National Association of Dental Plans (NADP) – nadp.org – Providing industry-standard statistics on PPO plan dominance and dental benefit trends.

- American Dental Association (ADA) – ada.org – The authoritative source for CDT codes and clinical procedure classifications.

- Fair Health Consumer – fairhealthconsumer.org – A non-profit resource for looking up UCR (Usual, Customary, and Reasonable) fees by zip code.

- Centers for Medicare & Medicaid Services (CMS) – cms.gov – Information regarding the integration of dental and medical insurance standards.

- Delta Dental Plans Association – deltadental.com – Data regarding network structures (PPO vs. Premier) and common policy exclusions.

- Journal of Dental Research – SAGE Journals – Research supporting the cost-effectiveness of preventive care in managed care models.