For most Americans, the anxiety associated with a dental appointment has less to do with the drill and more to do with the bill. It is a harsh reality that oral healthcare is frequently sidelined due to financial constraints. While medical insurance protects you from catastrophic financial loss, dental benefits are designed differently. They function more like a maintenance subsidy. This distinction is critical because understanding dental insurance and payment options is the only way to bridge the gap between the care you need and the price you can afford.

Table of Contents

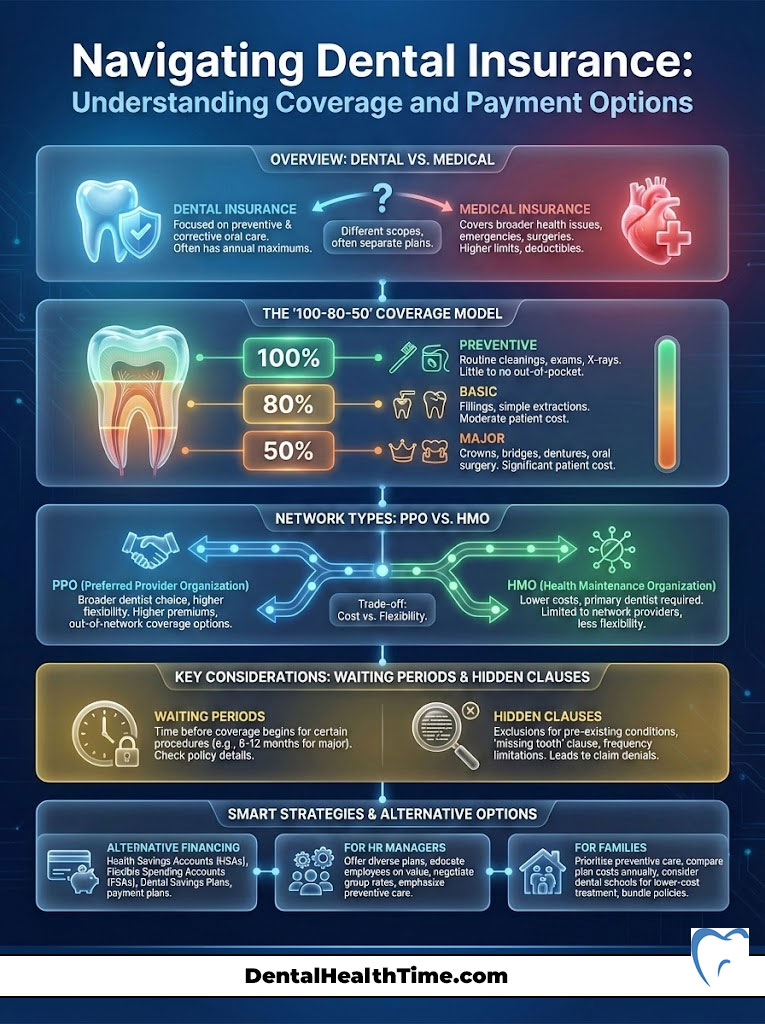

Understanding dental insurance and payment options involves navigating a complex ecosystem of benefit structures, network restrictions, and alternative financing tools. At its core, the system typically follows a “100-80-50” coverage model where preventive care is fully covered, basic procedures are partially subsidized, and major restorative work requires significant out-of-pocket contribution. Navigating this landscape effectively requires knowing the difference between PPO and HMO networks, understanding how to bypass waiting periods, and utilizing third-party dental payment options when insurance caps are reached.

The goal of this guide is to dismantle the confusion surrounding dental insurance plans USA. We will move beyond the jargon to expose the mechanics of coverage, the hidden clauses that lead to claim denials, and the modern financial tools that ensure your oral health never has to be compromised. Whether you are an HR manager evaluating benefits or a head of household trying to afford affordable dental care for your family, this comprehensive resource serves as your financial playbook.

Core Concept: How Dental Insurance Works and The Benefit Model

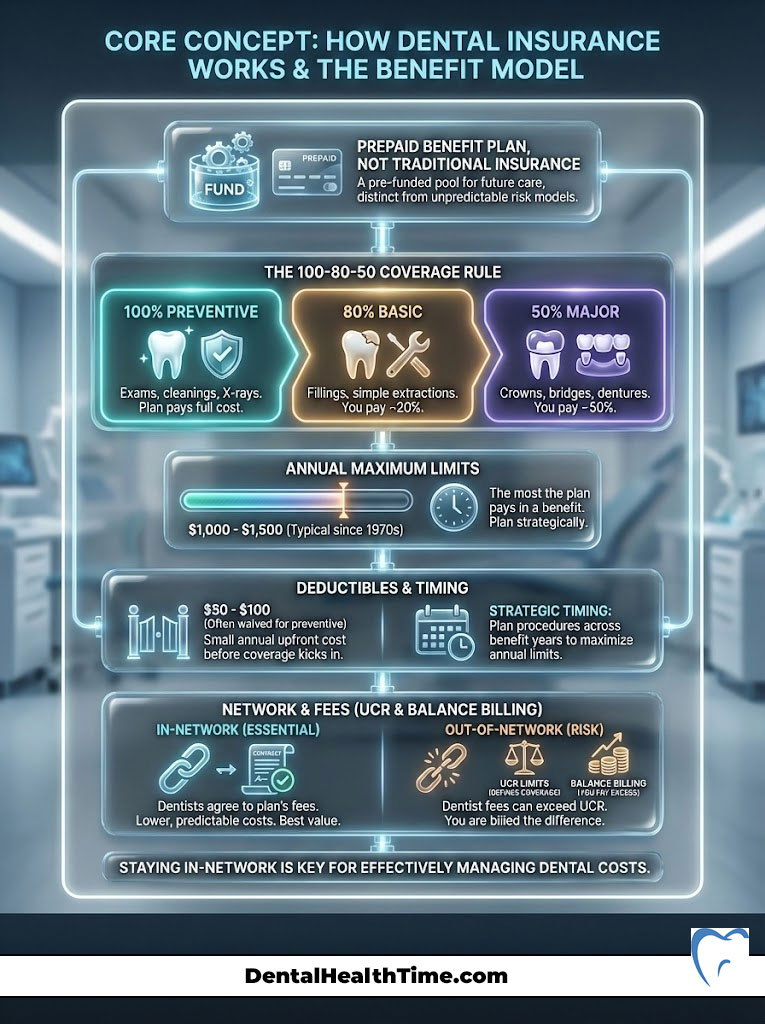

To master your benefits, you must first accept a fundamental truth. Dental insurance is not “insurance” in the traditional sense. It is a prepaid benefit plan. True insurance absorbs risk. If your house burns down, insurance pays to rebuild it regardless of the cost. Dental plans operate differently. They are designed to cover low-cost maintenance while capping their liability for expensive problems.

The Mechanics of the “100-80-50” Coverage Rule

Most dental insurance plans USA are built on a tiered structure known as the 100-80-50 rule. This formula dictates how much the insurance carrier pays versus your financial responsibility.

- 100% Preventive Care Coverage: This tier includes your biannual cleanings, routine exams, and bitewing X-rays. Carriers cover this fully because clinical data proves that $1 spent on prevention saves them money on future claims.

- 80% Basic Procedures Coverage: This category typically includes composite fillings, simple extractions, and periodontal maintenance. You pay the remaining 20% as co-insurance.

- 50% Major Procedures Coverage: This is where the bulk of patient frustration occurs. High-cost items like crowns, bridges, root canals, and dentures are usually covered at only 50%. You are responsible for half the bill.

Decoding the Annual Maximum and Deductibles

The most significant limitation in how dental insurance works is the annual maximum. This is the absolute ceiling on what the insurance company will pay for your care within a benefit year.

It is crucial to note that while the cost of dentistry has risen with inflation, the average annual maximum has remained stagnant at approximately $1,000 to $1,500 since the 1970s. Once the carrier pays out $1,500 on your behalf, you are financially on your own for the rest of the year. This makes strategic timing of procedures essential for maximizing benefits.

Dental insurance deductibles are the entryway costs you must pay before the plan contributes anything. Fortunately, these are usually low compared to medical insurance, hovering around $50 to $100 annually per person. In many Preferred Provider Organization (PPO) plans, the deductible is waived for preventive visits.

The Impact of UCR (Usual, Customary, and Reasonable) Fees

When you use an out-of-network dentist, your costs are calculated using the insurer’s UCR (Usual, Customary, and Reasonable) fee schedule. Insurance companies set a “UCR” price for every dental procedure based on regional (ZIP code) data, not on what your dentist actually charges.

For example, if your dentist charges $1,200 for a crown, but the insurance carrier’s UCR fee for that ZIP code is only $800, the insurer will calculate its 50% coverage based on the $800 amount. That means the insurance pays $400.

You are responsible for two parts: your 50% share of the UCR amount ($400) plus the difference between the dentist’s fee and the UCR ($400). In total, you pay $800 out of pocket. This practice — known as balance billing — is the primary reason why staying in-network is the cornerstone of affordable dental care.

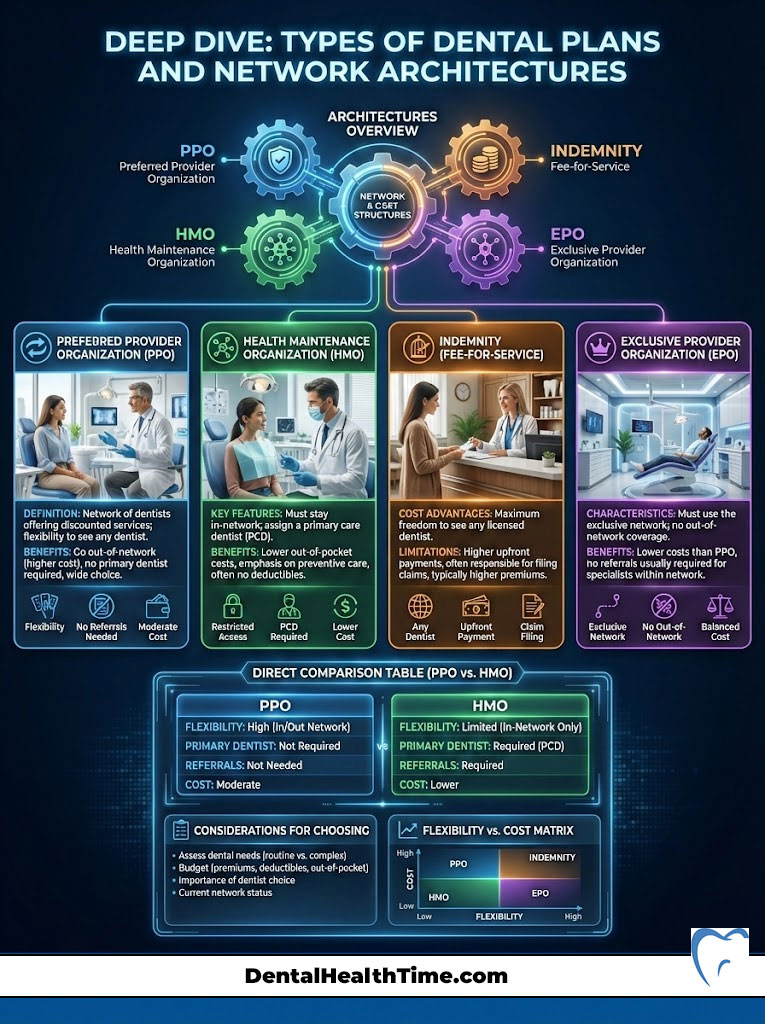

Deep Dive: Types of Dental Plans and Network Architectures

Selecting the right coverage requires analyzing how much flexibility you need versus how much premium you are willing to pay. The market is dominated by three main architectures: PPO, HMO, and Indemnity plans.

Preferred Provider Organization (PPO) Dental Plans

Dental PPO vs HMO dental plans is the most common comparison shoppers make. PPO plans are the most popular dental insurance plans USA because they strike a balance between choice and cost.

In a PPO, you have a network of dentists who have agreed to contracted rates. If you visit an in-network dentist, you get the benefit of these discounted fees. You can also visit out-of-network dentists, but your coverage percentage will likely drop, and you may be subject to balance billing. PPO plans almost always involve a deductible and an annual maximum.

Health Maintenance Organization (HMO / DHMO) Dental Plans

Dental HMOs, or Capitation plans, are the budget-friendly alternative. In this model, you must select a primary care dentist from a specific list. This dentist receives a fixed monthly fee to manage your care.

The advantage of a dental HMO is the cost structure. There are typically no deductibles and no annual maximums. Instead of percentage-based coverage, you pay a flat co-pay for services. For example, a crown might cost you a flat $300 regardless of the actual lab fee. However, the trade-off is rigid. If you see a provider outside the HMO network, you have zero coverage.

Indemnity and EPO Plan Structures

Indemnity plans, often called “traditional” insurance, allow you to see any dentist anywhere. The insurance company pays a percentage of the UCR fees, and you pay the rest. These plans offer the ultimate freedom but come with the highest premiums.

Exclusive Provider Organizations (EPO) are a hybrid. Like an HMO, you generally have no coverage out-of-network. Like a PPO, you may have a deductible and annual maximum. They are less common but often appear in employer-sponsored benefits packages.

Comparative Analysis: Dental PPO vs Dental HMO

To help you decide which dental payment options align with your needs, we have broken down the critical differences in the table below.

| Feature | Dental PPO (Preferred Provider Org) | Dental HMO (Health Maintenance Org) |

| Provider Choice | High flexibility. Visit any dentist. | Low flexibility. Must use assigned dentist. |

| Network Savings | Deep discounts in-network; less out-of-network. | Flat co-pays. No coverage out-of-network. |

| Premium Costs | Higher monthly premiums. | Lower monthly premiums (sometimes $0). |

| Annual Maximum | Yes (Typically $1,000 – $2,000). | No (Unlimited benefits). |

| Waiting Periods | Common for major restorative work. | Rare. Coverage is usually immediate. |

| Claim Paperwork | Filed by the dentist. | Minimal. Co-pays paid at the desk. |

| Best Profile | Patients who want to keep their current dentist. | Budget-conscious patients with major work needs. |

The “Fine Print”: Limitations, Exclusions, and Waiting Periods

Even the best dental insurance coverage comes with guardrails. Insurance carriers are businesses that manage risk, and they use specific clauses to protect their bottom line. Understanding these fine print details is essential to avoid unexpected bills.

Strategies for Navigating Dental Waiting Periods

A dental waiting period is a lockout time during which the insurer will not pay for specific procedures. The industry standard is usually:

- Preventive: No waiting period.

- Basic: 6-month waiting period.

- Major: 12-month waiting period.

This protects the insurer from “adverse selection,” where a patient buys insurance only because they immediately need a crown and then drops the policy. If you need urgent care, you must search specifically for dental insurance with no waiting period. These plans often have graduated benefits. For instance, they might cover only 20% of a root canal in year one, increasing to 50% in year two.

The “Missing Tooth Clause” Trap

This is perhaps the most shocking exclusion for new policyholders. The Missing Tooth Clause states that the policy will not cover the replacement of a tooth that was missing before the policy went into effect.

If you lost a tooth five years ago and now buy insurance hoping to get a bridge or implant, the claim will likely be denied under this clause. It is vital to check your policy document for this specific language if your goal is replacing old extractions.

The LEAT (Least Expensive Alternative Treatment) Clause

The LEAT clause allows the insurance company to downgrade your benefit to the cheapest viable option. A common example involves fillings. If you need a filling on a back molar, your dentist may recommend a composite (tooth-colored) resin for durability and aesthetics. The insurance company, citing the LEAT clause, may only pay for an amalgam (silver) filling because it is cheaper. You are then responsible for the difference in price between the silver and white filling.

The Importance of Pre-Treatment Estimates

To avoid disputes over dental insurance deductibles or denied claims, always ask your dental office to submit a “Pre-Treatment Estimate” or “Pre-Determination of Benefits.”

This is a formal request sent to the insurer before work begins. The carrier will respond with a document detailing exactly what they will pay and what your estimated share will be. This document is a powerful tool for planning your dental payment options and ensuring affordable dental care.

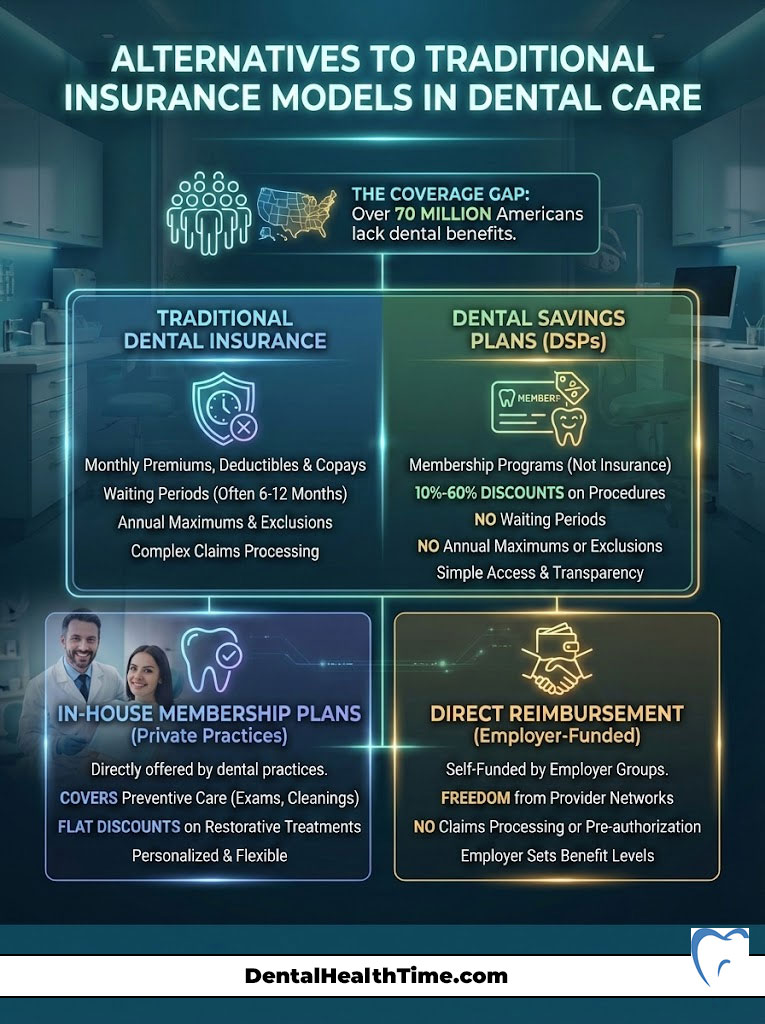

Alternatives to Traditional Insurance Models

For the roughly 70 million Americans without dental benefits, or for those whose needs exceed the $1,500 annual cap, the traditional insurance market may not be the answer. Modern dental payment options have evolved to fill this void.

Dental Savings Plans vs Insurance

Dental savings plans vs insurance is a debate gaining traction. A dental savings plan (or discount plan) is not insurance. It is a membership program. You pay an annual fee to gain access to a network of dentists who have agreed to reduce their rates for members.

The discounts typically range from 10% to 60%. The power of dental savings plans lies in their simplicity. There are no waiting periods, no annual maximums, and no exclusions for pre-existing conditions. If you need a root canal next week, a savings plan can be activated immediately to lower the cost.

In-House Membership Plans and Direct Primary Care

Many forward-thinking private practices are bypassing insurance companies entirely by offering in-house membership plans. In this model, you pay a monthly or annual subscription fee directly to the dental office.

This fee typically covers all preventive care (cleanings, exams, X-rays) and grants a flat percentage off all other treatments. This restores the doctor-patient relationship by removing the third-party payer who dictates treatment based on cost rather than clinical necessity. For patients without employer sponsorship, this is often the most transparent path to affordable dental care.

Direct Reimbursement Plans

A less common but highly efficient model is Direct Reimbursement. These are self-funded benefit plans set up by employers. The employee visits any dentist, pays the bill, and brings the receipt to the employer for reimbursement according to the company’s rules. This eliminates networks and complex claims processing, offering pure “fee-for-service” freedom.

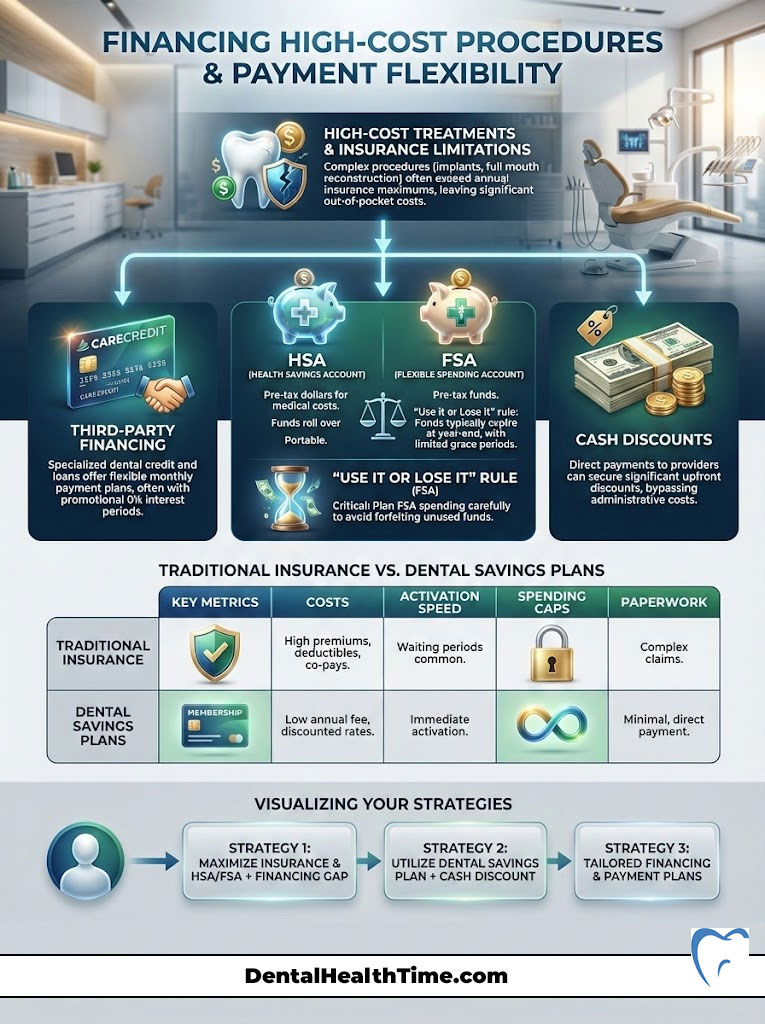

Financing High-Cost Procedures and Payment Flexibility

When facing a $20,000 treatment plan for full-mouth reconstruction or dental implants, a $1,500 annual insurance maximum is a drop in the bucket. This is where dental financing for procedures becomes the primary vehicle for access to care.

Third-Party Financing Tools

Specialized healthcare credit cards and lending platforms have become standard entities in the dental industry.

- CareCredit: The most widely recognized healthcare credit card. It allows patients to pay for treatments over time. The most attractive feature is the “deferred interest” promotional period (often 6, 12, or 18 months). If the balance is paid in full within this window, no interest is charged.

- Sunbit: A newer player focusing on high approval rates. Sunbit technology allows dental offices to approve patients for financing in roughly 30 seconds with a soft credit check that does not impact credit scores.

- LendingClub Patient Solutions: This entity is often used for larger loan amounts, such as dental implants or full-arch restorations. They offer extended terms with fixed monthly payments that fit into a household budget.

Leveraging HSAs and FSAs

Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) allow you to pay for dental insurance plans USA co-pays and procedures with pre-tax dollars. This effectively gives you a discount equal to your income tax bracket.

It is crucial to remember the “Use it or Lose it” rule associated with FSAs. Any funds remaining in the account at the end of the calendar year are typically forfeited. Smart patients schedule their major dental work in November or December to utilize these expiring funds.

Cash Discounts and Payment Terms

Never underestimate the power of direct payment. Many dental offices lose a significant percentage of their revenue to billing collections and credit card processing fees. Consequently, they are often willing to offer a “bookkeeping courtesy” or cash discount (typically 5%) if you pay the full estimated patient portion at the time of service. This is one of the simplest dental payment options to negotiate.

Comparison: Traditional Insurance vs. Dental Savings Plans

To clarify the dental savings plans vs insurance decision, review the financial mechanics below.

| Metric | Traditional Dental Insurance | Dental Savings Plan |

| Cost Basis | Monthly Premium ( 30−30-30− 60/mo) | Annual Fee ( 100−100-100− 150/year) |

| Activation Speed | Waiting periods apply (6-12 months) | Immediate activation (24-72 hours) |

| Spending Cap | Annual Maximum ( 1,000−1,000-1,000− 1,500) | No Annual Limit |

| Pre-Existing Conditions | Often Excluded (Missing Tooth Clause) | Accepted and Discounted |

| Network | Restricted (PPO/HMO) | Restricted (Participating Providers) |

| Paperwork | Claims, EOBs, Denials | No Paperwork. Discount at POS. |

Demographic-Specific Advice for Payment Options

Different life stages present different oral health challenges and financial constraints. Tailoring your strategy to your demographic profile ensures you are not overpaying for coverage you do not need.

Seniors and the Medicare Gap

One of the biggest shocks for American retirees is discovering that Original Medicare (Part A and Part B) does not cover routine dental care. It will only cover dental services if they are inextricably linked to a covered medical procedure (like an extraction prior to jaw radiation).

For this demographic, Medicare Advantage (Part C) plans are the primary solution. These private plans bundle dental, vision, and hearing benefits with Medicare coverage. Alternatively, seniors often gravitate toward dental savings plans because they cover the restorative work (dentures, implants) that becomes more common with age, without the caps of traditional insurance.

Freelancers and the Gig Economy

Freelancers lack the buying power of a large employer group, making private individual insurance expensive. For this group, the affordable dental care strategy often involves “stacking.” This means buying a low-cost preventive insurance plan for cleanings and pairing it with a high-limit Dental Savings Plan for any unexpected major work. Additionally, freelancers should look for dental insurance plans USA on the ACA (Affordable Care Act) marketplaces, though standalone dental plans there can be limited.

Families with Children and Orthodontics

For families, the focus is often on prevention and orthodontics. When evaluating plans, check for an “Orthodontic Rider.” This is a specific add-on that covers braces or clear aligners. Be aware that orthodontic coverage usually has a separate “Lifetime Maximum” (often $1,000 to $1,500) that is distinct from the annual maximum.

State-sponsored programs like CHIP (Children’s Health Insurance Program) mandate dental coverage for children, ensuring that income should not be a barrier to pediatric oral health.

Industry Trends and The Future of Dental Payments

The landscape of dental insurance plans USA is shifting under the weight of consumer demand and legislative pressure.

The Rise of Teledentistry

Teledentistry is emerging as a cost-effective triage tool. Instead of paying for an emergency exam just to be told you need a specialist, patients can use virtual consults. This lowers the barrier to entry and helps patients understand their dental payment options before they even step into the office.

Medical Loss Ratio (MLR) Legislation

A massive shift in “Authoritativeness” and trust is occurring due to MLR legislation. In states like Massachusetts, voters have approved measures requiring dental insurers to spend a specific percentage of premiums (e.g., 83%) on actual patient care rather than administrative costs and executive bonuses. This trend is expected to spread, forcing dental insurance plans USA to become more efficient and valuable to the consumer.

The Preventive-First Economic Model

Insurers and providers are aligning on the economic reality that prevention is cheaper than cure. We are seeing a trend where carriers are expanding preventive dental care coverage—sometimes covering 3 or 4 cleanings a year for high-risk patients (like those with diabetes or pregnancy) without counting it toward the annual maximum. This is a win-win: the patient stays healthy, and the insurer avoids paying for a root canal down the road.

Summary and Key Takeaways

Navigating Understanding dental insurance and payment options is about risk management and mathematical strategy. The “old way” of passively accepting whatever plan an employer offers is fading. The “new way” demands active engagement with your benefits.

To recap, your action plan for financial oral health involves:

- Identify Your Needs: Do you need maintenance (Preventive) or reconstruction (Major)? Choose PPO for flexibility or HMO for cost savings accordingly.

- Watch the Caps: Monitor your annual maximum closely. If you are near the limit, push non-urgent work to January to reset your benefits.

- Question the Wait: If you have urgent needs, prioritize dental insurance with no waiting period or switch to a discount plan.

- Finance Smartly: Use CareCredit or Sunbit to break large bills into manageable monthly payments without interest.

Ultimately, the most expensive dental care is the care you delay. By leveraging these dental payment options, you can ensure that financial barriers never force you to neglect your health.

Frequently Asked Questions (FAQ)

What is the difference between a dental deductible and a co-pay?

A dental insurance deductible is a one-time annual fee (e.g., $50) you must pay before your insurance contributes. A co-pay (or co-insurance) is the portion you pay for each specific visit or procedure after the deductible is met (e.g., paying 20% of the cost of a filling).

Does dental insurance cover dental implants?

Historically, no, but this is changing. Many modern dental insurance plans USA now classify implants as a “Major” service, covered at 50%. However, you must check for a “Missing Tooth Clause” which could deny the claim if the tooth was lost before coverage began.

Can I buy dental insurance just for braces?

You can, but you must look for a plan with an orthodontic rider. Be careful of waiting periods; many plans require you to be enrolled for 12 months before they will pay for orthodontics.

What happens if I reach my dental annual maximum?

Once the carrier pays out the maximum amount (e.g., $1,500), they stop paying for the rest of the benefit year. You are then responsible for 100% of the costs. It is often wise to delay non-urgent treatment until the benefits reset.

Are there dental payment options for people with bad credit?

Yes. Dental savings plans do not require credit checks. Additionally, many dental offices offer in-house membership plans that function like a subscription, regardless of credit history. Some financing tools like Sunbit also have high approval rates for lower credit scores.

How do I know if a dentist is in-network?

Use the insurance carrier’s “Find a Doctor” tool on their website. However, always call the dental office directly to confirm. Networks change frequently, and the website data may be outdated.

Can I use my HSA for teeth whitening?

Generally, no. The IRS considers teeth whitening a cosmetic procedure. HSA and FSA funds can only be used for procedures that treat a medical/dental disease or restore function, like fillings, crowns, or cleanings.

Why does dental insurance have a waiting period?

Insurers use dental waiting periods to prevent people from buying insurance only when they have an expensive problem and then cancelling it immediately after the claim is paid. This ensures the risk pool remains stable.

What is the best dental insurance for seniors on Medicare?

Since Original Medicare excludes dental, seniors often find the best value in Medicare Advantage (Part C) plans that include dental benefits, or standalone dental savings plans that offer unlimited usage for dentures and implants.

Do dental schools offer cheaper work?

Yes. Dental schools are a fantastic instance of affordable care. Procedures are performed by students under strict faculty supervision. Costs can be 30% to 50% lower than private practice fees, though appointments may take longer.

What does “full coverage” dental insurance actually mean?

“Full coverage” is a marketing term, not a literal one. It typically refers to a plan that offers benefits for Preventive, Basic, and Major restorative care (the 100-80-50 structure). No plan covers 100% of every procedure cost.

Disclaimer: The content provided in this article is for educational and informational purposes only and does not constitute financial, insurance, or medical advice. Insurance policies vary significantly by carrier and state. Always review your specific policy documents (EOB and Evidence of Coverage) or consult with a qualified insurance agent or dental professional before making financial decisions regarding your healthcare.

References:

- National Association of Dental Plans (NADP). State of the Dental Benefits Market.

- American Dental Association (ADA). Health Policy Institute Analysis of Dental Spending.

- Centers for Medicare & Medicaid Services (CMS). Dental Coverage in Medicare.

- Internal Revenue Service (IRS). Publication 502: Medical and Dental Expenses.