I recently sat down with a client in Alpharetta who was staring at a $1,400 quote for a single crown. He was completely baffled. He thought his coverage was solid until he read the fine print and realized his plan capped out at $1,000 annually. Finding the Top 5 dental insurance plans in Georgia requires more than just comparing monthly premiums; it demands a deep understanding of network density from Fulton County to Valdosta and a clear view of the “allowable amounts” carriers actually pay.

As a licensed insurance broker who has navigated the Georgia market for over 15 years, I have seen too many residents buy policies that look great on paper but fall apart when they sit in the dentist’s chair. Whether you are a freelancer in Savannah, a retiree in Rome, or raising a family in Marietta, the state regulations and provider availability here create a unique environment. This guide cuts through the marketing noise to identify the Top 5 dental insurance plans in Georgia based on real claims data, network strength, and policy value.

Quick Answer: Which Plan Wins?

For sheer network size, especially in rural areas, Delta Dental of Georgia is the standout choice. If you need immediate coverage for major work, Ameritas offers the best terms for waiving waiting periods. For seniors prioritizing loyalty rewards and increasing maximums, Humana takes the lead. Anthem BCBS is ideal for high annual maximums, while Cigna offers strong restorative benefits for families.

Navigating the Georgia Dental Market

Most national articles offer generic advice that fails when applied to the Peach State. The reality of dental insurance in Georgia is dictated by the disparity between Metro Atlanta and the rest of the state. In my experience dealing with the Georgia Department of Insurance (OCI) and reviewing carrier filings, I have noticed that a plan working perfectly in Midtown Atlanta might be useless in Tifton due to a lack of in-network providers.

The problem usually stems from UCR fees (Usual, Customary, and Reasonable). Dentists in affluent Georgia zip codes often charge fees significantly higher than what insurance carriers deem “reasonable.” If your plan lacks strong protection against balance billing, you pay the difference. This article maps out the journey from identifying the top carriers to understanding critical clauses like the Missing Tooth Clause and Network Adequacy.

You need to understand that Georgia is a “fee-for-service” dominant state in many rural sectors. This means dentists in smaller towns hold the leverage. They do not have to join insurance networks to keep their chairs full. Therefore, having a carrier with strong negotiation power is not just a luxury; it is a necessity.

Key Statistics: Dental Costs in Georgia

- Average Root Canal Cost (Atlanta): $1,000 – $1,400 (without insurance).

- Rural Provider Shortage: 25+ Georgia counties have fewer than 2 dentists per 10,000 residents.

- Average Annual Maximum: Most GA plans cap benefits at $1,500 per year.

- Orthodontic Costs: Braces in Georgia average $5,000 – $7,000 out of pocket.

- Premium Range: Individual plans in GA typically run between $25 and $60 monthly.

- Wait Times: New patient appointments in rural GA can have a 3-month lead time.

The Georgia Dental Environment: What You Need to Know First

Before we rank the specific plans, you must understand the mechanics of the local market. Georgia dental insurance is not a one-size-fits-all product because the cost of doing business for dentists varies wildly across the state.

The Atlanta vs. Rural Divide

In Metro Atlanta, you have access to hundreds of dentists. Here, the competition is high, and many dentists join PPO networks to get patients in the door. However, in rural Georgia, the dynamic shifts. I have clients in South Georgia who drive 45 minutes to see a dentist. In these areas, dentists are less likely to join low-reimbursement PPO networks because they have plenty of cash-paying patients.

This is where the distinction between a standard PPO dental plan and a “Premier” network becomes vital. A standard PPO might have zero dentists in a rural county, whereas a carrier with a Premier network will likely have coverage, albeit at a slightly lower reimbursement rate. If you live in a county like Echols or Taliaferro, a standard HMO or small PPO is practically worthless.

Understanding Georgia’s Cost of Care

Every insurance plan uses a fee schedule. In Georgia, this schedule is often tied to zip codes. A cleaning in zip code 30305 (Buckhead) is reimbursed at a higher rate than in 31021 (Dublin). However, if your dentist charges $150 for a cleaning and your dental insurance in Georgia only allows $90, you are responsible for that $60 gap unless you are seeing an in-network provider who has agreed to write off the difference.

This is why “balance billing” is such a critical concept. In-network dentists agree to accept the insurance company’s fee as payment in full. Out-of-network dentists do not. In a state with such economic disparity between counties, this contract between the doctor and the insurance company is your only shield against open-ended bills.

Broker’s Pro Tip: Before buying a policy, call your current dentist’s front desk. Do not ask, “Do you take this insurance?” They will almost always say yes, meaning they will file the claim for you. Instead, ask, “Are you an in-network provider for this specific plan?” This distinction can save you hundreds of dollars per visit.

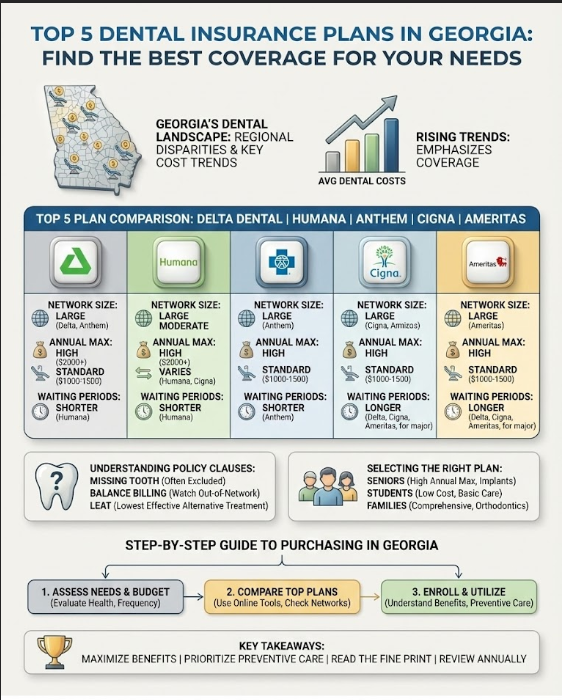

Detailed Review: Top 5 Dental Insurance Plans in Georgia

Based on fifteen years of policy review, claim satisfaction rates, and network stability, here is my professional assessment of the Top 5 dental insurance plans in Georgia. I have evaluated these not just on their brochures, but on how they actually perform when a claim is filed.

1. Delta Dental of Georgia (PPO Plus Premier)

Overview: Delta Dental is the heavyweight champion regarding network size. They are the market leader for a reason. In Georgia, their footprint is massive, covering nearly every county with at least one provider.

Deep Dive: The “PPO Plus Premier” structure is their secret weapon. The PPO network is smaller but offers deeper discounts (lower out-of-pocket costs). If your dentist is not in the PPO network, they might be in the Premier network. The Premier network is vast and acts as a safety net. While the discounts aren’t as aggressive as the PPO, the “Premier” status prevents the dentist from balance billing you beyond the allowable amount.

For example, if a procedure costs $100:

- In PPO Network: The negotiated rate might be $70. Insurance pays percentage of $70.

- In Premier Network: The negotiated rate might be $85. Insurance pays percentage of $85.

- Out of Network: You pay the full $100, and insurance reimburses you based on a low “customary” fee.

Broker’s Verdict: This is the best dental insurance in Georgia for residents in rural areas or those who travel frequently within the state. The probability of your dentist accepting Delta is higher than any other carrier. Their claims processing center in Alpharetta is also generally efficient, which reduces administrative headaches.

2. Humana Dental Georgia (Loyal Well-Being)

Overview: Humana takes a unique approach by rewarding longevity. They understand that dental insurance is often dropped after a year, so they incentivize you to stay.

Deep Dive: The “Loyal Well-Being” plan is structured to increase your benefits over time. In year one, your coverage percentage for basic fillings might be 40-50%. By year three, it often jumps to 70-80%. Furthermore, your annual maximum benefit typically increases each year you keep the policy active. This counters the inflation of dental costs effectively.

Another massive advantage for Humana in Georgia is their “open network” policy on certain plans. While they have a PPO network, their reimbursement rates for out-of-network dentists are often fairer than competitors. This reduces the sting if you absolutely must see a non-network provider.

Broker’s Verdict: This is the premier choice for dental insurance for seniors in Georgia. Retirees on a fixed income benefit from the increasing maximums and the inclusion of discounts for hearing aids, which Humana frequently bundles. The waiting periods are often reduced for those with prior coverage.

3. Anthem Blue Cross Blue Shield Georgia (Essential Choice)

Overview: Anthem is a powerhouse in the medical space, and their dental products leverage that administrative strength. They have significant bargaining power with hospital-based oral surgeons.

Deep Dive: The standout feature of the “Essential Choice” PPO is the high annual maximum options. While competitors stick to $1,000 or $1,500, Anthem offers plans in Georgia with limits up to $2,500. This is critical if you need a crown and a root canal in the same year. Additionally, they have strong coverage for composite (white) fillings on back teeth, which some carriers downgrade to amalgam (silver) rates.

Anthem also integrates well if you have their health insurance. Managing both policies through the “Sydney Health” app simplifies the administrative side of healthcare. Their network in the Atlanta metro area is dense, though it thins out slightly in the extreme northern mountains compared to Delta.

Broker’s Verdict: Best for total value and those who want a high ceiling on benefits. If you anticipate significant work, that extra $1,000 in annual benefits is a financial lifesaver. It is a robust plan for working professionals.

4. Cigna (Dental 1500)

Overview: Cigna is a strong contender for those who prioritize restorative work and consistent national coverage. They are particularly strong with corporate transfers who move in and out of Georgia.

Deep Dive: The Cigna Dental 1500 plan follows a classic 100-80-50 structure (100% preventive, 80% basic, 50% major). Their network is particularly strong in Metro Atlanta suburbs like Roswell, Marietta, and Sandy Springs. A key advantage is their negotiation power; Cigna’s contracted rates with dentists are often very competitive, meaning your 50% share of a crown is calculated on a lower base price compared to smaller carriers.

Cigna also offers decent transparency tools. Their online portal allows you to estimate costs before you go to the dentist, which is a feature many smaller carriers lack. This helps avoid “bill shock” after the procedure is done.

Broker’s Verdict: Best for families expecting major work like bridges or crowns. Their customer service and digital portal are also among the most user-friendly, making claims tracking simple. If you live in the suburbs, this is a top-tier option.

5. Ameritas (PrimeStar)

Overview: Ameritas is the flexible, aggressive option for people who need coverage yesterday. They are less conservative than the big “Blue” carriers.

Deep Dive: The “PrimeStar” series is famous for its approach to waiting periods. If you have had prior dental insurance in Georgia (even if it expired recently), Ameritas will often waive the waiting periods for major services entirely. Even without prior coverage, they offer “Day One” coverage for major services on some plans, albeit at a lower percentage that graduates up in year two.

Ameritas also has a unique “Dental Rewards” program. If you file a claim but use less than your annual maximum, they allow you to carry over a portion of that unused benefit to the next year. This is rare in the dental insurance world, which is typically “use it or lose it.”

Broker’s Verdict: Best for those switching plans who cannot afford a gap in coverage or need a waiting period waiver GA. They are also one of the few carriers that offer decent coverage for implants on individual plans.

Comparison Table 1: Top 5 Georgia Dental Plans at a Glance

| Carrier | Plan Name | Est. Monthly Cost (GA) | Annual Max | Deductible (Indiv) | Best Feature |

|---|---|---|---|---|---|

| Delta Dental | PPO Plus Premier | $35 – $55 | $1,000 – $1,500 | $50 | Largest Rural Network |

| Humana | Loyal Well-Being | $25 – $45 | Increases yearly | $50 (Lifetime) | Loyalty Rewards |

| Anthem BCBS | Essential Choice | $30 – $50 | Up to $2,500 | $50 | High Annual Max |

| Cigna | Dental 1500 | $35 – $50 | $1,500 | $50 | Restorative Coverage |

| Ameritas | PrimeStar | $40 – $60 | $1,000 – $2,000 | $50 | Next-Day Coverage |

Decoding the Fine Print: An Expert’s Guide to Policy Jargon

The brochure will always highlight the “No Deductible for Cleaning” feature, but that is not where you lose money. The financial danger lies in the clauses hidden on page 12 of the Certificate of Coverage. In Georgia, these clauses are strictly regulated, but they still exist.

The 100-80-50 Coverage Ratio Explained

Standard private dental insurance in Georgia operates on a 100-80-50 split.

- 100% Preventive: Cleanings, X-rays, and exams are fully covered (usually twice a year).

- 80% Basic: Fillings, extractions, and sometimes root canals (depending on the carrier) are covered at 80%. You pay 20%.

- 50% Major: Crowns, bridges, dentures, and complex oral surgery are covered at 50%. You pay half.

However, this split is based on the “allowable amount,” not necessarily what the dentist charges. If the dentist charges $1,200 for a crown and the insurance allows $800, they pay 50% of $800 ($400). You pay your 50% ($400) plus the difference if you are out of network. This “balance billing” scenario is the number one complaint I hear from clients who did not check their network status.

The “Gotchas” That Cost You Money

The Missing Tooth Clause

This is the most misunderstood exclusion in the industry. If you lost a tooth before you purchased your policy, the insurance company generally will not pay to replace it. They view this as a pre-existing condition. If you need a bridge to replace a tooth extracted three years ago, most plans will deny the claim. You must check for a “Missing Tooth Clause” waiver if this applies to you. Some carriers like Ameritas are more lenient here than others.

Waiting Periods vs. Immediate Coverage

Carriers protect themselves from “adverse selection”—people buying insurance only when they are in pain—by imposing waiting periods. Preventive care is almost always immediate. However, major services typically carry a 6 to 12-month wait. If you search for full coverage dental insurance Georgia no waiting period, you will likely find plans that offer immediate access but at reduced percentages (e.g., paying only 15% or 20% in the first year). It is a trade-off: pay more now for immediate access, or wait for better benefits.

Network Adequacy and Balance Billing

Balance billing Georgia dental laws protect consumers in emergency medical situations, but dental is different. If you go out of network, the dentist can legally bill you for the remaining balance. Network adequacy refers to the carrier’s legal obligation to provide enough doctors in your area. In rural Georgia, this is a frequent issue. If a carrier cannot provide an in-network dentist within a reasonable distance, you may be able to appeal for an “in-network exception,” though this is a complex administrative process that requires documentation.

The LEAT Clause (Least Expensive Alternative Treatment)

This is a subtle clause that affects your fillings. If you have a cavity on a back molar, you probably want a composite (white) filling. However, many insurance plans have a LEAT clause stating they will only pay for the “least expensive” option, which is an amalgam (silver) filling. If you choose the white filling, you pay the difference in cost. Anthem and Delta Dental’s higher-tier plans often cover white fillings on back teeth, which is a significant aesthetic and financial advantage.

Strategic Selection: Which Plan Fits Your Persona?

Selecting the best dental insurance in Georgia depends entirely on your stage of life and oral health history. A 22-year-old in Athens needs a completely different policy than a 65-year-old in Macon.

Best Dental Insurance for Seniors in Georgia

Seniors face unique challenges. Medicare does not cover routine dental care. For this demographic, I recommend plans that cover periodontal maintenance (deep cleanings) at a high percentage, as gum health often declines with age. Humana Dental Georgia and Anthem are strong here. Look for plans that include riders for dentures and implants, as these are high-cost items that can destroy a retirement budget. Seniors should also prioritize plans with lifetime deductibles rather than annual ones.

Affordable Dental Insurance for Students and Freelancers

If you are a gig worker in Atlanta or a student at UGA, you might not need heavy restorative coverage. You need affordable dental plans in GA that handle cleanings and emergency exams. In this case, a DHMO (Dental Health Maintenance Organization) might be viable. These plans have very low premiums (sometimes under $15/month) and no annual maximums, but you must stay within a very small network of providers. It limits your choice but saves your wallet. Cigna offers competitive DHMO options in urban centers.

Family Plans: Orthodontics & Braces for Kids in GA

Families often get blindsided by orthodontic limits. Orthodontics & braces for kids in GA are expensive. Most plans that cover braces have a separate “Lifetime Maximum” for orthodontia, usually capped at $1,000 or $1,500. Since braces can cost $6,000, the insurance is essentially a discount coupon, not a full payment method. Delta Dental and Ameritas often have the most comprehensive child orthodontic riders. Crucially, check if the plan covers “medically necessary” vs. “cosmetic” orthodontia, as this definition can vary by carrier.

Comparison Table 2: Coverage Suitability by Need

| Feature / Need | Best Carrier Option | Why? |

|---|---|---|

| Implants | Anthem BCBS / Ameritas | Specific riders and high annual maximums. |

| Orthodontics (Child) | Delta Dental / Ameritas | Separate lifetime max; comprehensive provider list. |

| No Waiting Period | Humana / Ameritas | Waived with proof of prior coverage. |

| Rural Access | Delta Dental | “Premier” network reaches underserved GA counties. |

| Low Premium | Cigna / Aetna (DHMO) | Lower monthly cost but restricted provider list. |

How to Buy and Enroll in Georgia

Once you have identified the right carrier, the purchase method matters. You generally have two paths, and choosing the wrong one can lock you into a plan that doesn’t start when you need it to.

Where to Buy Dental Insurance in Georgia

You can buy through Healthcare.gov (The Marketplace) during Open Enrollment. However, dental plans on the Marketplace are sometimes “embedded” with health plans, which can make deciphering the deductible tricky. Often, buying individual and family dental plans in GA directly from a private exchange or a broker is more advantageous. Private plans can be purchased year-round, not just during Open Enrollment, and often offer more robust standalone benefits. Private plans also tend to have better customer service options than exchange-based plans.

Step-by-Step Enrollment Guide

- Verify Your Dentist: I cannot stress this enough. Call your dentist and ask for their Tax ID or NPI number, then plug that into the insurance carrier’s provider search tool. This is the only way to be 100% sure they are in-network. Names can be similar; numbers are unique.

- Check the Formulary: If you care about having white fillings on your molars, check the plan’s exclusions. Many budget plans only pay for silver fillings on back teeth, leaving you to pay the upgrade fee. This information is found in the “limitations” section of the plan summary.

- Review the OCI Filing: For the diligent consumer, checking the Georgia Department of Insurance website can reveal if a carrier has a high volume of consumer complaints regarding claim denials. A carrier with a low complaint ratio is usually a safer bet for paying claims promptly.

- Understand the Effective Date: If you buy a plan on the 15th of the month, coverage usually starts on the 1st of the following month. Do not schedule an appointment for the 20th expecting coverage. Plan your care calendar accordingly.

Summary & Key Takeaways

Choosing among the Top 5 dental insurance plans in Georgia is about balancing risk and access. If you live in a rural county, Delta Dental Georgia is likely your only safe bet for network access. If you are a senior focused on long-term maintenance, Humana Dental Georgia offers the best loyalty incentives. For those needing immediate relief without waiting periods, Ameritas provides a vital escape hatch.

Remember, the cheapest premium often leads to the highest dental bill. Always prioritize Network Adequacy and the Annual Maximum over the monthly cost. Before your next appointment, pull out your policy, look for the “limitations and exclusions” page, and ensure you know exactly what your dental insurance in Georgia covers. It is the best way to keep your smile—and your wallet—intact.

Frequently Asked Questions

Which dental insurance plan is best for residents in rural Georgia counties?

For residents outside of Metro Atlanta, Delta Dental of Georgia’s PPO Plus Premier is the superior choice. Its unique ‘Premier’ network acts as a safety net in underserved counties where dentists often refuse standard PPO rates. This structure prevents ‘balance billing’ by ensuring the dentist accepts a negotiated fee, even if they aren’t in the smaller PPO network.

Can I find dental insurance in Georgia with no waiting period for major procedures?

Yes, but it requires strategy. Carriers like Ameritas and Humana frequently waive waiting periods for major services if you provide proof of prior creditable coverage. Alternatively, some Ameritas ‘PrimeStar’ plans offer ‘Day One’ coverage for major work, though they typically pay a lower percentage in the first year that increases over time.

What is the best dental insurance option for Georgia seniors on a fixed income?

Humana Dental Georgia’s ‘Loyal Well-Being’ plan is highly recommended for seniors. It rewards longevity with an annual maximum that increases every year you stay on the plan. This is critical for managing age-related costs like periodontal maintenance and dentures, which are not covered by standard Medicare.

How does ‘balance billing’ affect my out-of-pocket costs in Georgia?

Balance billing is a significant risk in Georgia’s ‘fee-for-service’ dominant rural sectors. If you see an out-of-network provider, they can bill you for the difference between their retail rate and the insurance carrier’s ‘allowable amount.’ To avoid this, always verify that your provider is strictly ‘In-Network’ rather than just ‘accepting’ the insurance.

Which Georgia dental plan offers the highest annual maximum for expensive restorative work?

Anthem Blue Cross Blue Shield Georgia’s ‘Essential Choice’ PPO is the leader for high-limit coverage, offering annual maximums up to $2,500. This is substantially higher than the Georgia market average of $1,500, providing a much-needed financial cushion for patients requiring multiple crowns or complex root canals in a single year.

Will my Georgia dental policy pay for a tooth I lost before I purchased the plan?

Most individual plans in Georgia contain a ‘Missing Tooth Clause,’ which excludes coverage for replacing teeth lost prior to the policy’s effective date. If you need a bridge or implant for a pre-existing gap, you must look for specific plans from carriers like Ameritas that may offer waivers or more lenient restorative terms.

Why did my insurance only pay for a silver filling when I requested a white one?

This is due to the ‘Least Expensive Alternative Treatment’ (LEAT) clause. Many budget-friendly Georgia plans only reimburse for the cost of an amalgam (silver) filling on back molars. If you prefer composite (white) fillings, you must pay the difference unless you choose a higher-tier plan from Anthem or Delta Dental that specifically covers white fillings on all teeth.

Are dental implants covered by individual insurance plans in Georgia?

Implants are generally considered a ‘Major’ service and are only covered by high-tier PPO plans. Ameritas and Anthem BCBS are among the few in the Georgia market that offer robust implant riders. Be prepared for a 12-month waiting period and ensure the cost doesn’t exceed your plan’s annual maximum.

How do I ensure my specific dentist is actually in-network for a new plan?

Do not rely on verbal confirmation that they ‘take’ the insurance. Ask the office for their NPI (National Provider Identifier) or Tax ID number. Use this unique identifier in the carrier’s online provider search tool to confirm they are an ‘In-Network’ participant for the specific plan tier you are purchasing.

What is the average cost of braces for children in Georgia, and does insurance cover it?

Orthodontics in Georgia typically cost between $5,000 and $7,000. Most family dental plans treat this as a ‘Lifetime Maximum’ benefit, usually capped at $1,000 or $1,500. Essentially, the insurance acts as a discount rather than full coverage. Delta Dental and Ameritas offer some of the most consistent orthodontic riders for children.

Is it better to buy dental insurance through Healthcare.gov or a private broker in Georgia?

Buying through a private broker or exchange is often better for dental. Private plans are available year-round, whereas Marketplace plans are usually tied to Open Enrollment. Furthermore, private standalone plans often provide higher annual maximums and better ‘Network Adequacy’ than the embedded dental plans found on the Marketplace.

What are the typical premiums for quality dental insurance in the Georgia market?

For a comprehensive PPO plan in Georgia, expect to pay between $35 and $60 per month. While DHMO plans are available for under $20 in urban centers like Atlanta or Savannah, they offer very restricted provider networks and are often impractical for residents in rural counties with fewer dentists.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or medical advice. Insurance premiums, network availability, and policy terms in Georgia are subject to change by carriers and state regulators. Always consult with a licensed insurance professional or verify specific plan details directly with the carrier before enrolling in a policy.

References

- Georgia Department of Insurance (OCI) – https://oci.georgia.gov/ – Official state regulator for insurance filings, consumer complaints, and network adequacy standards in Georgia.

- Delta Dental of Georgia – deltadentalins.com – Provider of the PPO Plus Premier network data and regional claim processing information for GA.

- American Dental Association (ADA) Health Policy Institute – ada.org – Source for dental cost statistics, UCR fee data, and provider density maps for Georgia.

- Healthcare.gov (The Marketplace) – healthcare.gov – Information regarding embedded vs. standalone dental plans and Georgia enrollment periods.

- National Association of Dental Plans (NADP) – nadp.org – Industry data regarding dental insurance trends, 100-80-50 coverage structures, and consumer utilization.

- Humana Georgia Plan Filings – humana.com – Technical details on the “Loyal Well-Being” plan structure and senior-specific loyalty rewards.

- Georgia Dental Association – gadental.org – Insights into the Georgia dental market, rural provider shortages, and fee-for-service trends.